An 18 month exit planning timeline is a structured, compressed schedule that guides a small business owner through the financial and operational improvements needed to prepare a company for sale within a year and a half. This timeline prioritizes high-impact fixes that maximize valuation and minimize deal friction during buyer due diligence.

Why 18 Months Is the Minimum Viable Exit Timeline for SMBs

An 18-month exit planning timeline is a structured, compressed schedule that guides a small business owner through the financial and operational improvements needed to prepare a company for sale within a year and a half. This timeline prioritizes high-impact fixes that maximize valuation and minimize deal friction during buyer due diligence.

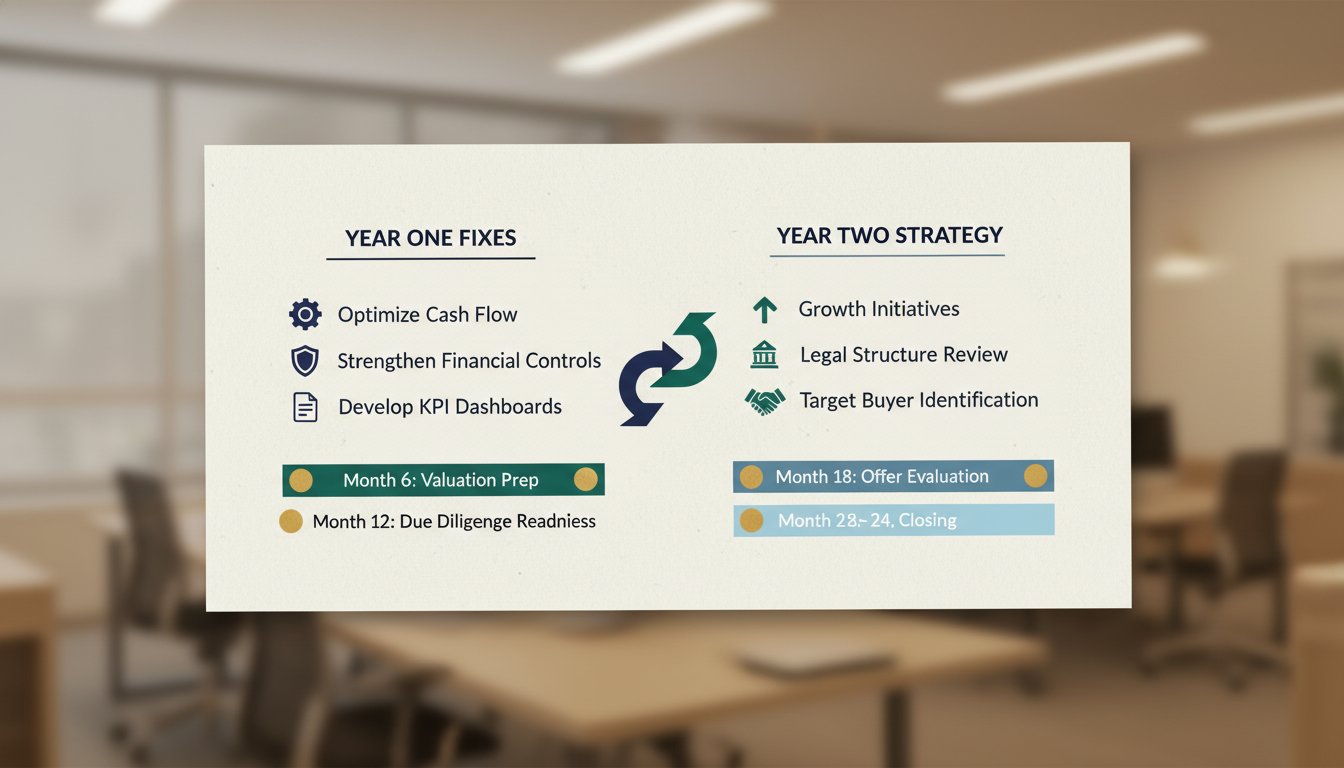

1 However, an 18-month compressed timeline is viable for SMB owners who focus exclusively on the fixes that buyers actually scrutinize. The key is sequencing: year one targets financial cleanup and tax optimization, while year two addresses structural gaps that would otherwise kill a deal.

The difference between a three-year plan and an 18-month plan is not the quality of preparation—it is the scope. A longer timeline allows for organic revenue growth, multi-year tax strategies, and gradual operational changes. A compressed timeline forces owners to prioritize the 20% of improvements that drive 80% of valuation impact.2

Buyers during due diligence focus on three things: verified financials, clean legal structures, and documented operations. An 18-month timeline is sufficient to deliver all three if the owner starts with a clear checklist and avoids common distractions like rebranding or unnecessary capital expenditures.

| Phase | Months | Priority Actions |

|---|---|---|

| Year One | 1–12 | Revenue recognition, chart of accounts cleanup, tax structure, QofE |

| Year Two | 12–18 | Contract audit, IP assignment, CIM preparation, data room |

Year One: Fixing the Low-Hanging Financial Levers

The first twelve months of an 18-month exit planning timeline focus on financial hygiene. Buyers will reconstruct your financial statements back three to five years, so year one is about making those statements auditable.

Start with revenue recognition. If your business recognizes revenue on a cash basis, convert to accrual accounting. Buyers value predictable, recurring revenue streams—not lumpy cash deposits that obscure true performance. For a typical service business with $2 million in annual revenue, this conversion alone can increase valuation by 0.5x to 1.0x EBITDA.3

Next, clean up the chart of accounts. Many SMBs have dozens of miscellaneous expense categories that make financial analysis impossible. Consolidate to 15-20 standard accounts. Buyers and their accountants need to compare your margins against industry benchmarks, and they cannot do that if "office supplies" includes a $15,000 server purchase.

Finally, identify and eliminate owner-specific expenses. Personal vehicles, family members on payroll, country club memberships—these must be removed from the P&L or properly classified as add-backs. A buyer will discount your EBITDA by the full amount of any personal expense they discover during due diligence.

Month 6-12: Cleaning Up Books and Tax Structures

By month six, the financial cleanup should be complete. Months six through twelve focus on tax structure optimization and historical accuracy.

Review your entity structure. Many SMBs operate as LLCs taxed as S corporations, which is generally optimal for sale. However, if you have multiple entities—an operating company, a real estate holding company, and a management company—consider consolidating. Buyers prefer simple structures. A buyer will typically require a single acquisition entity, and unwinding multi-entity structures during due diligence can delay closing by 60-90 days.4

File amended tax returns if necessary. If your historical returns contain errors or aggressive positions, correct them now. Buyers will request three to five years of tax returns during due diligence, and any discrepancy between your tax returns and your financial statements is a red flag that triggers deeper investigation.

Consider a quality of earnings (QofE) report. This is a third-party analysis that adjusts your historical financials to reflect normalized, sustainable earnings. A QofE prepared six to twelve months before listing gives you time to address any adjustments the buyer would otherwise make themselves—often at a lower valuation.

Month 12-15: Building Your Exit-Ready Financial Dashboard

At the twelve-month mark, shift from cleanup to presentation. Buyers evaluate businesses based on forward-looking metrics, not just historical performance. Your financial dashboard should tell a story of predictable, growing cash flows.

Build a rolling 12-month cash flow forecast. This shows the buyer that you understand your business's cash conversion cycle and can predict working capital needs. For a typical SMB, the cash conversion cycle ranges from 30 to 60 days.5 A buyer will model this themselves, but a well-prepared forecast demonstrates management sophistication.

Create a customer concentration report. Buyers want to see that no single customer represents more than roughly 10% of revenue. If one client represents 40% of revenue, expect a 20-30% valuation discount compared to a business with balanced revenue distribution.

Document your pricing methodology. Buyers want to understand how you set prices, how often you raise them, and what drives margin changes. A documented pricing strategy with annual escalation clauses signals pricing power, which directly supports higher valuation multiples.

Year Two: Addressing the Structural Gaps Buyers Flag

Year two of the 18-month exit planning timeline addresses the structural issues that cause deals to fall apart during due diligence. These are harder to fix than financial cleanup, which is why they come second.

Review all customer and vendor contracts. Buyers will request every material contract for the past three years. Look for change-of-control clauses that allow counterparties to terminate upon sale, automatic renewal terms that lock in unfavorable pricing, and missing signature pages. A single missing contract can delay closing by weeks.

Audit your intellectual property. If your business uses proprietary software, processes, or branding, confirm that the IP is properly assigned to the company—not to the founder personally. Many SMB owners develop IP before forming the company and never execute an assignment agreement. This is a deal-killer for technology buyers.

Standardize employee documentation. Buyers will review employment agreements, non-compete clauses, and equity grants. Ensure every employee has a signed agreement, that non-competes are enforceable in your state, and that any equity compensation is properly documented. For a business with 15 employees, missing paperwork on even two key employees can reduce the offer price by 5-10%.

Month 15-18: Preparing the CIM and Management Interviews

The final three months before listing focus on the confidential information memorandum (CIM) and management presentation. These documents are the buyer's first impression of your business.

The CIM should be 30-40 pages covering business overview, market position, financial performance, growth strategy, and risk factors. Do not write this yourself—hire an M&A advisor or investment banker. A professionally written CIM signals that the seller is sophisticated and serious, which attracts higher-quality buyers.

Prepare for management interviews. Buyers will want to meet the founder, the CFO, and key operational leaders. These interviews are structured diligence sessions where buyers probe for weaknesses. Practice answering questions about customer concentration, competitive threats, and historical financial anomalies.

Create a data room with organized documentation. The data room should include financial statements, tax returns, contracts, employee records, IP documentation, and any regulatory filings. Organize by category with clear file names. A disorganized data room signals operational chaos and invites deeper scrutiny.

The 90-Day Sprint: Final Adjustments Before Listing

The last 90 days before listing are for fine-tuning, not major changes. Any structural fix attempted in this window risks creating more problems than it solves.

Focus on working capital optimization. Reduce accounts receivable days outstanding and negotiate extended payment terms with key suppliers. A cleaner working capital position means the buyer needs less cash to operate the business post-close, which supports a higher purchase price.

Resolve any outstanding legal or regulatory issues. Open litigation, unresolved tax audits, or zoning violations must be closed or clearly disclosed. Buyers will discount their offer by the full potential liability of any unresolved matter, not just the expected cost.

Prepare a 90-day post-close transition plan. Buyers want to see that the founder will remain available for a smooth transition. A written transition plan covering customer introductions, vendor relationships, and operational handoffs signals professionalism and reduces the buyer's perceived risk.

Your Next Step

Schedule a 30-minute diagnostic call with a fractional CFO or M&A advisor to assess your current financial readiness against the 18-month exit planning timeline. Bring your most recent 12 months of financial statements and a list of your top five customers. The advisor will identify which year-one fixes apply to your business and whether the compressed timeline is realistic for your specific situation. [email protected]

Footnotes

-

https://theexceptionalplan.com/exit-planning-for-small-businesses-exit-strategy-development-the-exceptional-plan/ ↩

-

https://www.bizbuysell.com/learning-center/article/exit-planning-timeline/ ↩

-

https://smaartcompany.com/blog/exit-planning-small-business ↩

-

https://www.eastcoastadvisoryteam.com/post/exit-planning-for-business-owners-the-complete-guide-to-getting-out-on-your-terms ↩

-

https://www.exitadvisors.org/knowledge-center/exit-planning-costs-small-business ↩